Hard-Hit Retailers Hope That ‘Revenge Shopping’ Will Be A Thing

The Retail industry is hoping for 2021-22 to be a breakout year. For example, in the US, National Retail Federation (NRF) CEO Matt Shay stated that, “…healthy consumer fundamentals, pent-up demand and widespread distribution of the vaccine will generate increased economic growth, retail sales and consumer spending.” Therefore, the NRF is forecasting that retail sales will grow between 6.5 percent and 8.2 percent in 2021-22.

As retailers announce last year’s 4Q and full year results, we’re seeing what we expected based on 2Q and 3Q performance. Fast moving consumer goods retailers (“FMCG”: principally grocers) and big-box general merchants like Walmart (+6.7%) and Target (+21%) had a good 2020-21, as shoppers focused on basic needs during lockdown. Fashion and specialty merchants tell a different tale. Fashion-oriented companies like Nordstrom (-31%) and Kohl’s (-20%) took big hits to their top lines. Specialty retailer Michaels achieved an almost-normal lift (+4%), while PetSmart achieved better than 5.5% revenue growth (pets were the beneficiaries of the fact that humans couldn’t hang out with other humans during most of the last year).

It stands to reason then that retailers that raced ahead last year are looking to increase their dominance, while those that have fallen behind seek to catch up. Undoubtedly, the NRF’s guidance is welcome news to everyone. And that optimism was buoyed last week in the US by the March jobs report.

The question is, are consumers ready to make the rosy outlook come true?

The usual methods for projecting performance may not help much. As all the RSR partners have opined in the last few months, there’s nothing about the last year that would or should ever be considered “normal”. That’s a problem for anyone who is trying to forecast 2021-22. It’s not a safe bet to use last year as the baseline. Can the industry gain any insight from all that “exogeneous data[1]” that we at RSR keep writing about? I’m not sure how a planner is supposed to translate all the fear and loathing that we see in social media these days into something that can help determine demand.

Planners are nonetheless tasked with coming up with numbers. This is where a couple of social (not social media, but the real society) factors come into the picture.

The first is something that observers are calling “revenge shopping”. In its March 12th digital edition, WWD described revenge shopping this way: “Revenge shopping, the phenomenon where consumers spend money on items and experiences that they have felt deprived of during the pandemic, may be on its way to the U.S. ‘with a vengeance’….”

This isn’t merely wishful thinking. In his book entitled Future Luxe: What’s Ahead for the Business of Luxury, author Erwan Rambourg (who spent many years in retail as a Marketing Manager in the luxury industry, notably for LVMH), stated that “so-called ‘revenge buying,’ which started in mainland China very rapidly after COVID-19 came under control and as early as late March <2020> was a tangible reason not to temper enthusiasm about future prospects… the appetite for luxury, especially with the younger generation, is alive and kicking.” The thinking goes, if it happened in China, it will happen elsewhere.

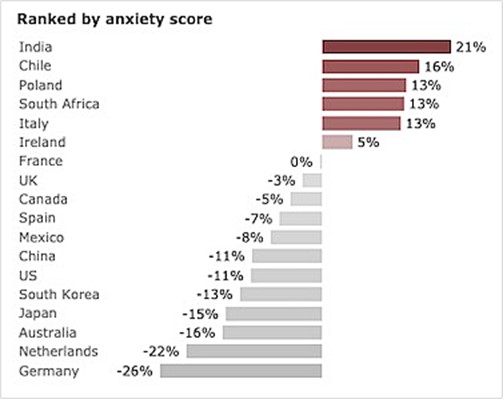

But every silver lining has a cloud, and that cloud is “consumer anxiety”. Global consulting firm Deloitte recently published the results of its latest State Of The Consumer Tracker study. When consumers were asked to agree or disagree with the statement, “I’m more anxious than I was last week” only last week, here’s what the results showed:

Clearly, people in many parts of the world and particularly those in consumer-oriented economies are coming out of their confinements. That’s good news! But for many, anxiety lingers. For example, the study found that in the US, as many consumers are worried about their finances as they are in getting the coronavirus (about ½ of those surveyed).

Nonetheless, the assessment is more optimistic than otherwise. Deloitte U.S. Consumer Industry Leader Anthony Waelter summarized it this way: “The stress of the pandemic is shifting from personal safety to financial security as we turn the corner and vaccinations become more readily available. Yet, despite a rise in financial stress related anxiety, consumer intent to maintain or increase discretionary spending is also on the rise, demonstrating more confidence in the recovery. With the passing of the stimulus bill recently, and checks beginning to roll out, businesses may very well expect to see consumer spending trends accelerate.”

What can retailers make of all of this? While it’s better than getting the Ouija board from the attic, “revenge shopping” and “consumer anxiety” aren’t factors usually considered in the business plan. But for some retailers and their supplier partners, that’s exactly what must happen this year and possibly next. We’re in for a wild ride.

[1] Non-transactional data used to help determine demand, such as consumer sentiment, the weather, competitive, market metrics, etc.